Company Update / Banks / IJ / Click here for full PDF version

Author(s): Jovent Muliadi ;Anthony

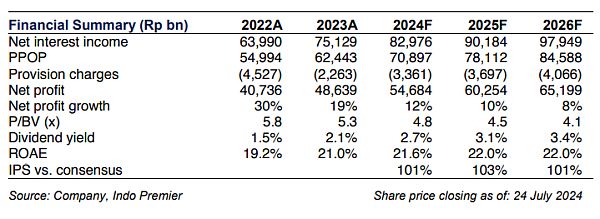

- 's 1H24 net profit of Rp26.9tr (+11% yoy/+9% qoq) was in-line with estimates driven by strong PPOP and benign CoC.

- NIM up by +10/20bp yoy/qoq to 5.7/5.8% in 1H24/2Q24 amid higher LDR (76% in 2Q24 vs. 69/75% in 2Q23/1Q24) above its target of 5.5-5.6%.

- Strong loan growth (+16% yoy) was coming from all segment while LAR also improved (-260/-20bp yoy/qoq). Maintain Buy with unchanged TP.

1H24 results: in-line from strong loan growth and better asset quality

posted 1H24 net profit of Rp26.9tr (+11% yoy/+9% qoq), in-line at 49/50% of our/consensus FY24F estimates. PPOP grew by 11% yoy (+5% qoq) driven by NII and non-II at +8/12% yoy (+1/-6% qoq) and mild opex growth (+5% yoy/-10% qoq). Provision rose by +13% yoy (-63% qoq) which translated to credit costs of 0.3% in 1H24 (0.5/0.4% in 1H23/1Q24), in-line with its FY24F CoC guidance of 0.3-0.4%.

Better NIM in 2Q24 driven by higher LDR

Overall NIM improved by +10/20bp yoy/qoq to 5.7/5.8% in 1H24/2Q24 amid higher LDR of 76% in 2Q24 vs. 69/75% in 2Q23/1Q24. Nevertheless, it maintains FY24F NIM guidance unchanged at 5.5-5.6% as it recently hiked its TD rate by c.75bp in Jun24. Deposit grew by +5% yoy (flat qoq), driven by (+6% yoy/+1% qoq) while TD was slower (+2% yoy/-3% qoq) partly due to TD rate cut in Mar24.

Robust loan growth from all segments

Loan growth was robust at +16% yoy (+2% qoq) driven by all segments. The growth was led by corporate (+20% yoy/flat qoq) - largely investment loan from minerals and down-streaming, followed by consumer (+14% yoy/+4% qoq), SME (+13% yoy/+4% qoq) while commercial was the slowest (+8% yoy/+2% qoq). However, it maintains FY24F loan growth target at 9-10%, which we think is too conservative.

LAR continued to trend down while coverage was maintained

NPL stood at 2.2% in 2Q24 vs. 1.9% in 2Q23/1Q24 while total LAR continued to trend down in both yoy and qoq basis at 6.4% in 2Q24 from 9.0/6.6% in 2Q23/1Q24. LAR coverage stood at 71% in 2Q24 vs. 62/72% in 2Q23/1Q24.

Maintain Buy with unchanged TP as its ROAE continued to deliver

We continue to like and maintain our Buy call following the strong result; worth noting that its 2Q24 ROAE has reached 24%, a 10 year high. currently trades at 4.7x P/BV vs. 10Y avg of 3.7x but we believe that the premium is justified. Risk to our call is weaker NIM from competition in lending.

Sumber : IPS